To those who are more financially conservative, they may frown upon the use of credit card and see it as an evil that tempts one towards over-spending and debt. It is indeed a double-edged sword – master it and a credit card can give you endless benefits in terms of accruing air miles and cash rebates, or you might always fall into becoming a slave to it. The latter can be a scary thought, where interest payments compounds every month to make the initial bill become an unmanageable mountain of debt. If you’ve been sucked into this black hole or are falling into it, do you know that the mighty credit card could be a powerful ally as well?

0% Balance Transfer

Balance transfer facility is usually offered as a complementary service on a credit card for customers to transfer the outstanding balance on one credit card to another credit card. This service can be very useful when you want to consolidate multiple credit card bills under just one credit line. This not only help you to focus on clearing just one single debt but also greatly reduces the amount of interest you need to pay.

Let us look at a scenario where John, who currently owns 2 credit cards from Bank A and Bank B. He has accumulated a $5,000 debt on each card. Both banks charge an annual interest of 25% and a late payment charge of 3% on outstanding balance.

Using these information, we can calculate the amount John will have to pay in a year.

($5000 X2) + 25% interest = $12,500. (excluding late payment charges)

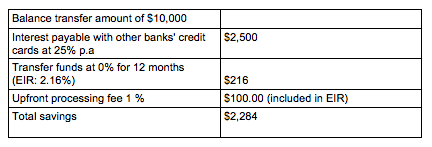

However, if John chooses to use a balance transfer utility such as the one by ANZ, he’ll get to save a substantial amount of money:

*Figures have been simplified for illustration purposes. The effective interest rate (EIR) of 2.16% p.a. is inclusive of the processing fee, based on a minimum payment of 3% for the first 5 months and full payment of the loan amount before the expiry of the 6th month.

As you can see from the table above, that’s a lot of interest savings just by changing your payment method! But we need to reiterate that savings on interest payments do not mean you have cleared your debt. You will still need to clear your outstanding amount but using the 0% balance transfer definitely helps to save you much money from interest payments.

Prevent Late Payment Charges

You can save yourself from paying unnecessary late payment charges if you can manage your monthly cashflow properly. Much like a business, cashflow can determine the solvency of the individual.

Let’s go back to John’s scenario: he owes a debt of $10,000 but only have $2,000 to spare each month for repayment. He’ll need to be extra alert of the due date for this bill and pay the $2,000 from his pocket first. For the rest of the $8,000, he can use another bank’s credit card to pay. This will help to extend his $8,000 outstanding amount by a 30-day’s grace from late fees.

Timing is key here and you have to make sure you pay the $2,000 diligently each month or the numbers will just pile up with the compounding interest. Repeat the routine with another bank’s credit card on the next month. Credit cards from different banks have different billing cycle so use this to your advantage.

Remembering these billing cycles can be challenging and you might lose track. The main point is to try to clear them as soon as you can or use the 0% balance transfer method so that you only have one bill to look after.