Singapore money: Positive outcomes from personal debt

Enjoy Compare’s Mark Hall looks at the problems caused by consumer debt, and gives practical advice on how to keep your financial affairs on the straight and narrow.

You cannot dispute that personal debt is a problem for some people in Singapore. While the huge majority are able to manage their financial affairs, there are some for whom money remains a problem and will always need a helping hand.

There’s also a small yet significant number living in the ‘here and now’, for whom personal debt is a lifestyle choice. This so-called ‘Western disease’ of accumulating loans and personal finance for one’s own sake – often going beyond the means to reasonably pay it back – could conceivably pose dangers to our economy if allowed to spiral out of control.

We argue that this is a poor choice to make, and have spoken to people who have shared their real-life financial situations with us, to prove there are positive choices that allow you to live debt-free.

Millions of us live with no financial problems at all, and credit cards and loans such as those offered on our website are of enormous benefit to many. Debt needn’t be a burden – there can be positive outcomes if addressed sensibly.

How to get out of debt

The facts about debt in Singapore

The truth is, debt in Singapore isn’t really as bad as the rest of the world. While improbable amounts of both secured and unsecured personal debt that caused the global financial collapse a few years ago, the island’s government took – and are still taking to this day – stringent measures to ensure that we remain as protected as possible from huge debt defaults.

While the debt of one person is manageable, that of thousands and millions left a financial black hole that US and European banks bandied about like a hot potato until financial institutions began to collapse, realising that they had lent so much money they were never going to get it back.

Debt and overspending brought whole countries to their knees, yet Singapore remained relatively isolated? Why was that?

The Monetary Authority of Singapore (MAS) holds a tighter reign over our banks and financial institutions than in the rest of the developed world. While in the US and elsewhere, banks are effectively able to make their own rules, our banks are strictly controlled to ensure relative financial caution and effective operations. MAS tends to act before problems occur, while other regulators habit a habit of reacting far too late.

We’re not without our problems, however.

Debt in Singapore has been called the country’s “Achilles’ heel”, and has led to MAS to impose stricter financial controls in the last year to mitigate any future problems. New measures have capped mortgage lending so repayments are no more than 60 per cent of a borrower’s monthly income. That’s to prevent potential problems where a customer falls behind on repayments and the loan goes bad – exactly the problem that brought down the US banks.

Credit card lending is also more tightly regulated, with minimum incomes required, and new cards refused to those who are more than 60 days in arrears with their accounts. Once again, a smart move to prevent debt being repaid with even more debt. We’re right behind that – credit cards are about sensible money management, not for building up a huge bill.

However, it can be easy to fall into problems:

Positive outcomes: Wendy’s story

Wendy L works in an office for a well-known corporation. Aged 25, she’s an office supervisor, but found herself overspending on everyday essentials and her mortgage, a situation not helped by a liking for the finer things in life.

“I’ve got a good flat and a well-paid job,” Wendy told us. “The mortgage is fine, but manageable most months. The trouble is, I used to love shopping, restaurants and taking holidays.

“Before I knew it, my credit card was maxed out, I was overdrawn in the bank, and right on course to miss a mortgage payment. The thought of that filled me with dread.

“It wasn’t a conscious decision to fall into debt. It just happened, slowly but surely over a few months. That’s what happens when you take your eye off the ball financially,” she warns.

Wendy admits that she fell into the trap that catches out some people with credit cards: It’s neither a loan, nor is it free money to freely spend until you’ve reached your credit limit. The best way, she now realises, is to pay off your credit card bill in full every month, so you get the benefit of members’ offers, but none of the interest or late repayment fees.

“I did what I should have done when it first started being a problem,” Wendy said. “I went and spoke to my bank. I’m so glad I did.”

Making an appointment with her personal account manager changed Wendy’s life for the better. She’s not the first person with a good income and solid repayment history they’ve seen struggling with their money, and certainly won’t be the last, and they forwarded a plan to help her back on her feet.

“The first thing they did was convert by bank overdraft and other debts into on single loan at an affordable interest rate. That immediately freed up hundreds of dollars a month that I was paying out just to stay afloat.

“Then I economised like crazy. No meals out. No fancy clothes. And certainly no holidays to Bali and Hong Kong.”

It took “one, mad, hard-working year” to get out of debt, and Wendy says she feels lucky that the situation didn’t get out of control.

“I’m able to use my credit card with confidence now,” she tells us, “It’s a great one with all kinds of brilliant rewards, but I always make sure it’s paid off in full every month. No more borrowing.”

Wendy tells us she’s “ashamed” of that period of her life, but is now happy to talk about it two years down the line if it helps people realise the dangers of over-spending.

“My message is that you shouldn’t bottle up your debt. Your bank doesn’t want you to default – go and talk honestly to them and they’ll help you out.”

There are some simple lessons from Wendy’s tale of financial recovery:

• Pay off your entire credit card bill in full every month

• Don’t spend more that you can reasonably afford to pay off every month

• If you are in difficulties, don’t keep your problems to yourself as they will only get worse. Speak to your bank or credit card provider for immediate, helpful solutions

How to get out of debt fast

Getting better at handling money

We’ve learned so far that over-stretching your finances can be a recipe for disaster.

But is Singapore as a whole getting better at handling its money? The latest figures certainly point in that direction.

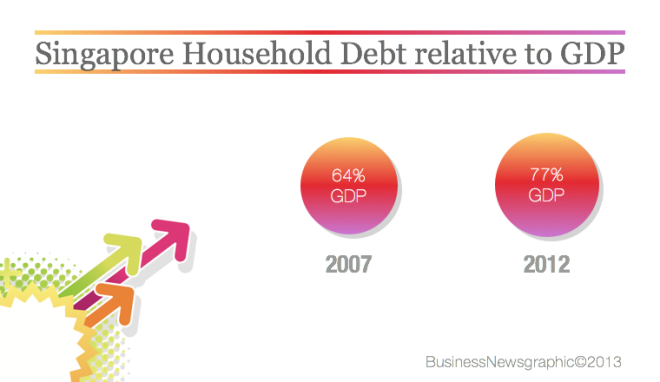

According to statistics released by our Parliamentary Estimates Committee earlier this year, the total average household debt in Singapore (that’s loans, credit cards, mortgages etc) currently stands at 2.1 times household income.

That may sound like a lot to you, but you have to remember that mortgages are usually extremely long-term secured loans that inevitably stretch the household income multiplier, otherwise nobody would be able to buy property.

The second point about this potentially eye-watering ratio is that is has steadily gone down in the last decade or so. According to MAS, household debt in the first decade of the 21st Century was a staggering 2.6 times income, which was clearly unsustainable. Part of that is down to falling interest rates, but tighter lending conditions and better personal financial management have also played a part.

The point the Parliamentary Committee makes about Singapore’s personal debt is that – unlike in other countries around the world – the people carrying the burden have enough income for it not to be a problem. With our monthly average salary currently sitting at about $6,000, most financial experts see this as no problem for now.

UOB’s financial expert Vincent Tan told The Straits Times in January: “As long as there is no sudden spike in interest rates – and the hike is expected to be very gentle – most people should be able to continue servicing their loans.”

Singaporeans have learned vital lessons about money management over the years, and has applied it to their own personal experience.

Positive outcomes: Geoffrey’s story

Geoffrey Y sells cars for a living, but it wasn’t always that way. In his 30s now, he studied medicine in the UK, dropped out of his course once he realised that it wasn’t the life he expected, and found his niche as a salesman.

“I like to think I’m a pretty good one too,” he says, “I pay a lot for my flat, but it’s worth every cent.”

We worked out how much of Geoffrey’s income goes out on his mortgage and he was surprised to learn it was 58%.

“That’s incredible. I knew it was high, but had no idea. Luckily I’ve got enough left over at the end of the month to live comfortably,” he laughs.

One of the things that alarmed Vincent about his college days in London was an almost casual attitude toward personal debt.

“Virtually everybody on my course had a mountain of debt before they’d even reached the end of their teens,” he said. “All were living in the moment, and said they’d pay it all back once they got into a decent paying job. But that would have been years away.”

Vincent admits he got drawn into the lifestyle, and returned home owing “a few thousand dollars”.

What to do? Vincent didn’t really have a plan, except to pay back what he owed, while finding a job and somewhere to live away from his parents’ home. He accepted a job in a car dealership from a friend, expecting it to last only a couple of years, and is still there ten years later.

“It only took me a couple of years to get out of debt,” said Vincent, “and it was my own hard work.”

Married now with a daughter, Vincent has a refreshing attitude towards money.

“I only spend what I have, but that’s OK because I’ve got plenty.”

He opens his wallet to show three credit cards from well-known Singapore banks. One is gold, the other – he is at pains to point out – is platinum. Laying them out on the table in front of me, he explains what each one is for.

The first, he says, is the most important. It’s the one he uses virtually every day for his car, and offers 18% discount on fuel at selected petrol stations. He drives all over the island and beyond to meet clients and suppliers, so it’s vital.

“What’s the balance on that?” I ask, already knowing the answer.

“Zero,” he beams, “Paid it off last month and every month.”

The second – platinum – card is Vincent’s luxury item, giving him discounts and loyalty points on overseas travel, and he and his family travel a lot.

“Zero,” he says.

And the third? Everyday use, discounts and rebates on everyday shopping, eating out, and night clubs. (“I don’t use that reward any more. I might change this card”).

Total balance: Zero. He’s worked hard in the last decade, and his only debt to his name pays for the roof over his head. As long as the money coming in is higher than the money going out, he’s happy with his lifestyle choice.

Vincent’s advice to fellow Singaporeans is this: Debt’s not a dirty word if you control it. Make sure you manage your money, and you’ll live a happy life.

‘I’m in serious debt, what should I do?’

Debt happens for many reasons: Losing a job, illness, gambling, poor personal planning. It’s easy to condemn those who owe money, but that doesn’t do anything to help their situation.

Instead, there are several choices the indebted person can take which should result in positive outcomes, and there’s no reason that once the root causes and the effects of debt are addressed that they can’t return to living a ‘normal’ financial life.

Without sounding too much like at 12-Step Debt ‘Anonymous’ recovery programme, the first step is to realise the grip that debt has over you and to make immediate moves to prevent the situation getting any worse.

The problem for many (and this is one that anybody who has ever been through an ‘Anonymous’ recovery programme will testify to) is that they often leave it until ‘rock bottom’ before looking for help. A debt of a few hundred dollars can easily multiply into thousands simply because they are too scared to admit it to either family or the bank.

Lesson one: Admit to yourself and your bank you have a problem

Believe me, the battle is already half won at this point.

But there is so much more you can do. As we’ve said before (see Wendy’s story above), speak to your bank immediately, and give them an open and honest appraisal of your predicament. They don’t want to call in a bad debt, nor do they want to lose you as a customer, so they will put steps into place to help you financially.

For example, bank and credit debts may be converted into cheaper loans, and they might suggest certain safeguards to protect your account.

It’s not just your bank who can help. Approach Credit Counselling Singapore (http://www.ccs.org.sg/), a non-government charity set up specifically to help out people with severe debt problems. They offer counselling and practical help to get people out of debt, and change their spending habits to help them onto the straight and narrow. Supported by the banks, courts and major credit bureaus, it’s as if you’ve got everybody behind you.

Their philosophy is that debt isn’t just about money, it requires an attitude change as well. Practical advice puts things in place to help deal with creditors, and to control outgoings. They’ll also recommend other organisations in Singapore that might give specialist help depending on your situation.

Steps you should be taking:

• Tackle your debt head on and in full

• Admit you have a debt problem to a loved one

• Admit you have a debt problem to your creditors

• Agree a plan with your creditors or bank to solve your problem

• Seek help from counselling or a support group

• Change the lifestyle that got you into problems

Steps you should avoid:

• DON’T gamble your way out. There’s no big win out there, just more debt

• DON’T lie to yourself or to others about your debts. Only 100% honesty will help you

• DON’T ask for a bailout from friends or family without addressing the root cause of your problem. Time and again people have just gone deeper back into debt

• DON’T take out a high interest loan just because they’ll lend you some cash – that’s just digging a deeper hole

The only way out of severe debt is by making a fresh start, and that takes a little courage. However, we can attest to the fact that many Singaporeans have taken this advice and now lead far happier lives. Here’s one such story:

Positive Outcome’s: Timothy’s story

Timothy finished his NS a few years ago and says he went “very, very wild with money”.

“I didn’t even know what I was doing, it was like a madness,” he said of his tens of thousands built up on gambling, spending and living the high life.

“The thing is that my salary covered my spending most of the time, by which I mean I could make all the minimum payments with cents to spare, and I just got wilder and wilder.”

It came to a head when his girlfriend found a pile of unopened bank statements hidden in a drawer and demanded answers. Opening up, he also admitted to borrowing money from friends, and was getting advances on his pay from a sympathetic boss just to make ends meet.

“I was ashamed,” he said of that day, “but it was also the best thing that could have happened. I wish I had owned up months before, but I would never have had the courage.”

Timothy owned up to all his debts, and made an appointment with the charity Credit Counselling Singapore. They offered practical advice, and also gave him the address of a counsellor who could help with his gambling and spending addictions.

“That was the most important part,” Timothy says, looking back. “Of course, I went straight to my banks and told them everything, and they were only too happy to help me out.

“It was the counselling that helped me the most, though.”

Timothy is resigned to the fact that he’s spent thousands, and only hard work over a number of years will wipe out that debt, but he’s happy with that situation.

“It could have been so much worse,” he says. “I spoke to the right people, and they’ve helped me get out of debt. I’m getting there – just give me another 21 months and seven days… not that I’m counting!”

He nods across to Grace, now his fiancée. “She’s the one with the financial sense, and I’m learning the most from her. She doesn’t owse anybody a cent, not even on her credit cards.”

Credit card debt help

Can I live debt free?

Virtually everybody carries debt of some kind or another. As we’ve discussed, the largest portion of indebtedness we all carry at some time or another is a mortgage on our home, but many don’t actually see that as debt per se, more a necessary bill as much as paying for your electricity every month.

While the number of people in Singapore carrying significant debt is mercifully small, it’s still necessary to offer every type of help available. The CCS says they see around 1,600 new cases of credit card debt every year, so we cannot deny there is a small, yet not crippling problem for some people.

For many of the millions living on this island, money is not a problem, and they have no reason to worry about paying their bills each month.

Debt-free living within your means is a possibility for all of us. As the people we spoke to in the production of this article kindly reminded us, good financial management is all about honesty – both with yourself and the people around you.

That means the world of consumer credit cards, and all the benefits that they bring should be seen not as a problem, but as an opportunity and a means to enjoy your life.